Here are the top 3 stocks we are watching for swing trades going into the…

Carson DavisMarch 17, 2024

Skip to main content

Skip to main content

In spread trading, investors often create positions that involve buying one financial instrument and simultaneously selling another related instrument.

The goal is to profit from the relative price movements between the two assets. If the trader is net short in a spread, it means that the position’s value would increase if the price of the asset they sold (short position) decreases more than the asset they bought (long position) or if there is a general decline in the overall market. These are examples of debit spreads and credit spreads.

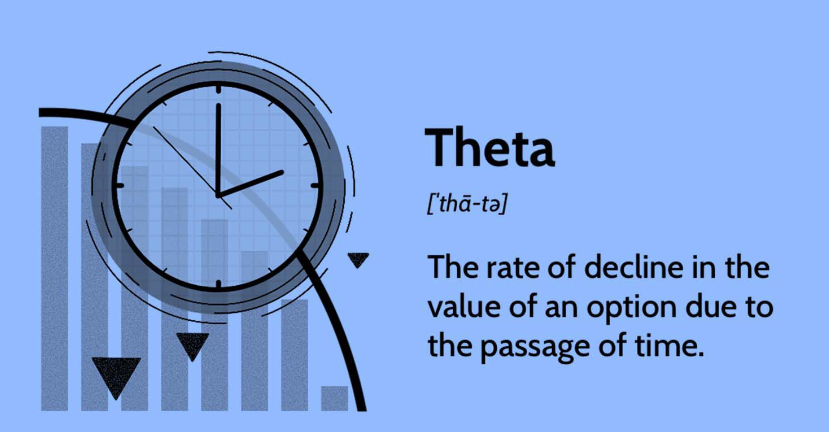

To summarize, the trade would be receiving money to take the trade. This is considered a “credit” trade. A credit spreads most advantageous aspect is being able to leverage theta.

Theta is an options greek that makes contracts lose value (premium) over time as the options contract comes closer to expiration.

A credit spread is a financial trading strategy that involves simultaneously entering two positions in the options market. This strategy is called a credit spread because the trader receives a net credit upfront when establishing the position. The two common types of credit spreads are the bull put spread and the bear call spread.

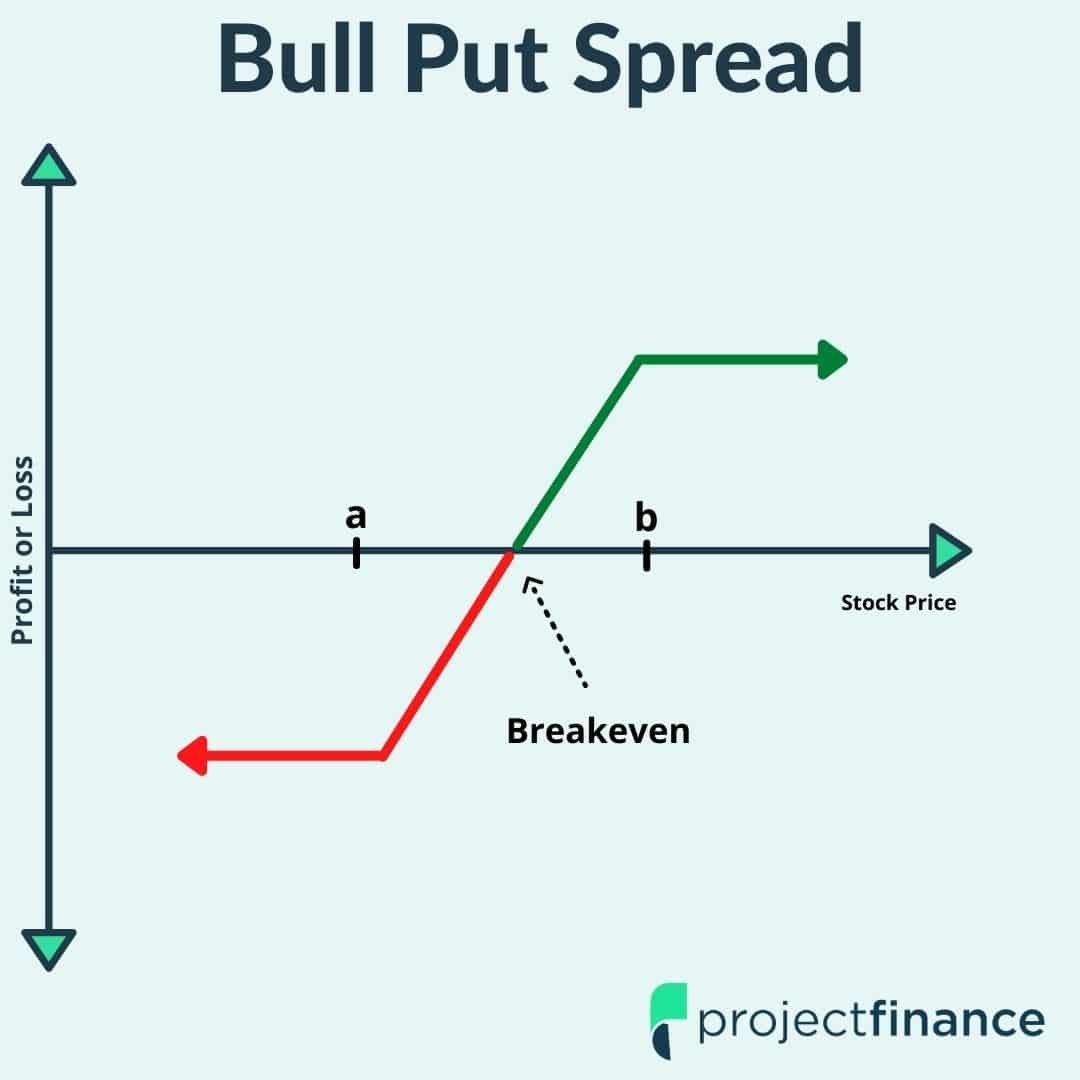

Bull Put Spread:

Objective: The trader expects the price of the underlying asset to rise or, at the very least, remain above a certain level.

Execution: Sell a Put Option: The trader sells (writes) a put option with a higher strike price. Buy a Put Option: Simultaneously, the trader buys a put option with a lower strike price.

Outcome: The trader receives a premium (credit) for the option they sold.

The maximum loss is limited to the the difference in strike prices minus the initial premium received. The maximum gain is limited to the premium received.

Risk/Reward Profile: Limited risk, limited reward. Profit is realized if the underlying asset’s price remains above the higher strike price.

Bear Call Spread:

Objective: The trader expects the price of the underlying asset to fall or, at the very least, remain below a certain level.

Execution: Sell a Call Option: The trader sells (writes) a call option with a lower strike price. Buy a Call Option: Simultaneously, the trader buys a call option with a higher strike price.

Outcome: The trader receives a premium (credit) for the option they sold.

The maximum loss is limited to the the difference in strike prices minus the initial premium received. The maximum gain is limited to the premium received.

Risk/Reward Profile: Limited risk, limited reward. Profit is realized if the underlying asset’s price remains below the lower strike price.

In both types of credit spreads, the trader aims to profit from the time decay of options and seeks to keep the net premium received as profit if the options expire worthless. It’s important to note that while the potential gains are limited, the potential losses are also capped, making credit spreads a defined-risk strategy. However, traders should carefully consider the risk and reward dynamics before engaging in any options trading strategy.

Theta, also known as time decay, is one of the Greeks in options trading that measures how much the value of an option will decay over time. Being net short in a trade, especially when it comes to options strategies, can allow traders to leverage theta to their advantage. Here’s how traders can use being net short to benefit from time decay:

Credit Spreads (e.g., Bull Put Spread, Bear Call Spread):

Objective: Credit Spreads allow traders to take advantage of time decay by selling options (being net short) with the expectation that the options will lose value over time.

Time Decay Benefit: As time passes and the options approach expiration, the value of the options sold (short options) decreases due to time decay.

Profit Mechanism: If the options expire worthless or are bought back for a lower price than initially sold, the trader profits from the net premium received.

Short Strangles and Straddles:

Objective: Traders can sell both a call and a put option with different strike prices (being net short) to profit from the decay in the options’ time value.

Time Decay Benefit: Time decay erodes the value of both the call and put options, potentially resulting in a profit.Profit Mechanism: If the underlying asset’s price remains within a certain range and both options expire worthless, the trader keeps the premium received.

Naked Option Selling:

Objective: Traders may sell (write) options without holding a corresponding position in the underlying asset.

Time Decay Benefit: By being net short options, traders can profit as the options lose value over time.

Profit Mechanism: If the options expire worthless or can be bought back for a lower price, the trader benefits from time decay.

Iron Condors:

Objective: Traders can construct an iron condor by selling both a put spread and a call spread, creating a neutral strategy that benefits from time decay.

Time Decay Benefit: Both the put and call spreads profit from time decay as long as the underlying asset’s price remains within a certain range.

Profit Mechanism: If the options expire worthless or can be bought back for a lower price, the trader profits from the net premium received.

It’s important to note that while being net short in a trade allows traders to benefit from time decay, it also comes with risks. The potential for unlimited losses in certain strategies, such as naked option selling, means that risk management is crucial. Traders should carefully consider their risk tolerance, have exit strategies in place, and monitor positions regularly. Additionally, understanding the interplay of other option Greeks (such as delta and gamma) is important for effective options trading.

© 2024 Davis Capital Research. All Rights Reserved.

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator