Skip to main content

Skip to main content

Options Greeks

What are options greeks and why do I need them for options trading strategies?

By definition:

Options Greeks are a set of risk measures that help traders and investors understand the sensitivity of options prices to various factors.

These factors, known as Greeks, provide insights into how changes in market conditions, such as price movements, volatility, time decay, and interest rates, affect the value of options and must be understood before deploying any options trading strategies.

Most important greeks:

The most common and important greeks are delta, theta, and gamma. All three have massive implications on the pricing of your options contract and must be understood before deploying any options trading strategies.

Check out my weekly trading digest:

Breaking Down Each Options Greek:

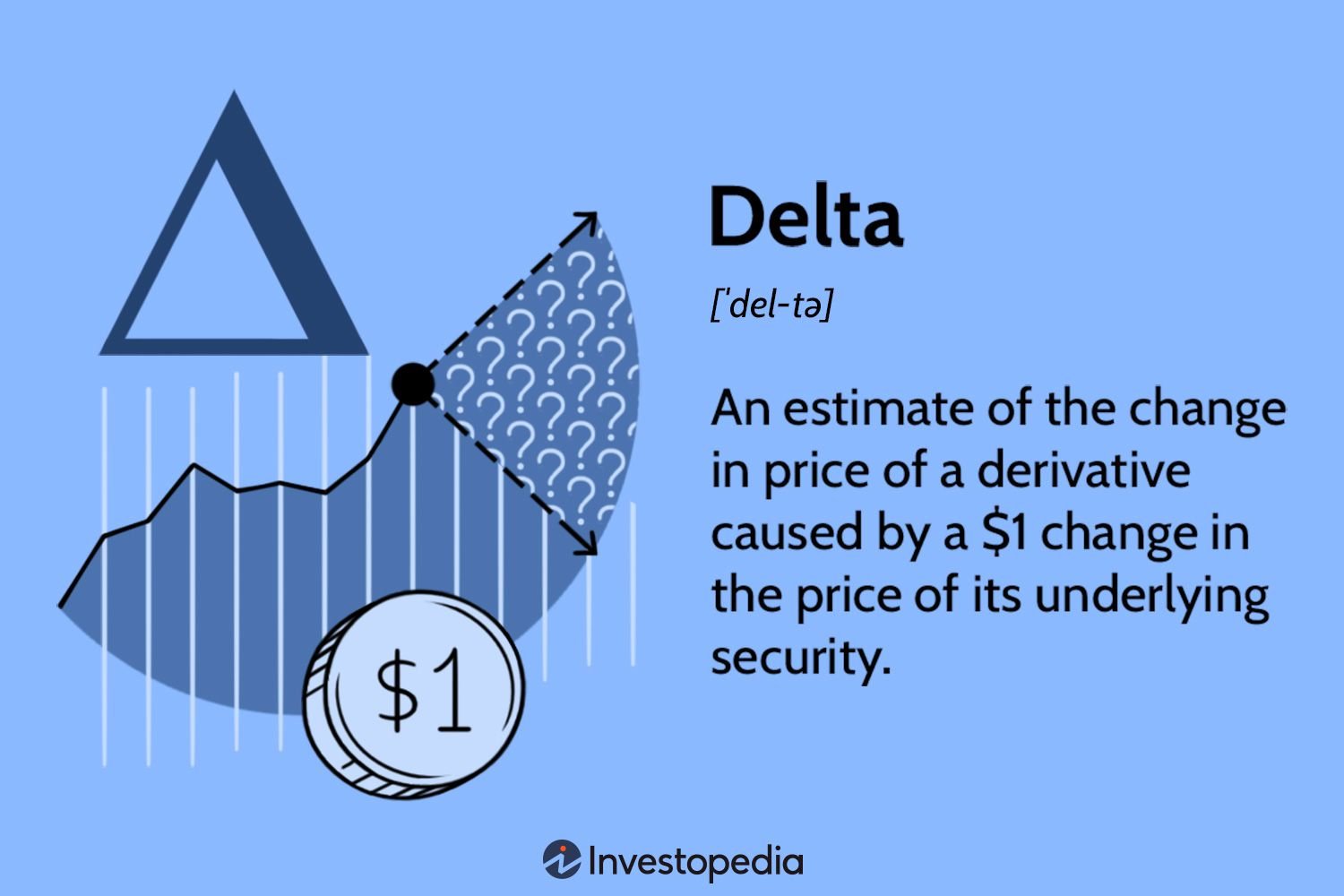

Delta:

Delta is one of the Greeks in options trading that measures the sensitivity of an option’s price to changes in the price of the underlying asset. It quantifies how much the option price is expected to change in response to a $1 change in the price of the underlying stock or index.

Delta is expressed as a numerical value between 0 and 1 for call options and between 0 and -1 for put options.

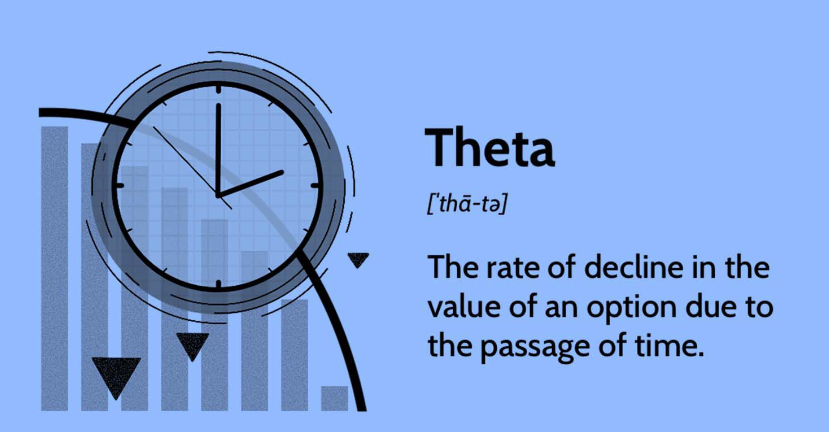

Theta:

Theta is one of the Greeks in options trading, and it measures the sensitivity of an option’s price to the passage of time. Also known as time decay, theta quantifies how much the value of an option is expected to change as each day passes, assuming all other factors remain constant.

Theta is expressed as a negative value because options tend to lose value as time passes.

Gamma:

Gamma is one of the Greeks in options trading, and it measures the rate of change of an option’s delta in response to changes in the price of the underlying asset.

In other words, gamma quantifies how much the delta of an option is expected to change for a $1 move in the price of the underlying stock or index.

Vega:

Vega is one of the Greeks in options trading, and it measures the sensitivity of an option’s price to changes in implied volatility. Implied volatility is a market’s expectation of how much an underlying asset’s price is likely to fluctuate in the future.

Vega quantifies the expected change in the option price for a 1% change in implied volatility.

Rho:

Rho is one of the Greeks in options trading, and it measures the sensitivity of an option’s price to changes in interest rates. Rho quantifies how much the option price is expected to change for a 1% change in the risk-free interest rate.

Mastering the Greeks for your options trading strategy:

1. Educate Yourself:

Read books and educational resources dedicated to options trading. Some popular books cover both the basics of options and more advanced topics related to Greeks.

Understand Each Greek:

Break down each Greek and understand its individual impact on options pricing. For example, understand how Delta represents price sensitivity to changes in the underlying asset, how Theta accounts for time decay, and so on.

Interactive Learning:

Use options trading platforms or simulation tools that provide real-time data and allow you to experiment with different scenarios. This hands-on experience can deepen your understanding of how Greeks behave in different market conditions.

Explore Sensitivity:

Analyze how each Greek changes under different market conditions. Understand how Delta, Gamma, Theta, Vega, and Rho evolve with changes in the underlying price, volatility, time to expiration, and interest rates.

Learn the Interactions:

Understand how the Greeks interact with each other. For example, know how Gamma affects Delta, how Theta accelerates as expiration approaches, and how Vega influences option prices in response to changes in implied volatility.

Apply Greeks to Strategies:

Practice applying Greeks to different options trading strategies, like long calls and puts for example. Understand how adjusting positions based on changes in Delta, Gamma, Theta, Vega, or Rho can impact risk and reward.

Options Greeks Educational Videos:

Options Greeks: Full Breakdown

Delta:

Call Options Delta:

Delta for call options typically ranges from 0 to 1.

A delta of 0 means the call option is out of the money and has a very low probability of expiring in the money.

A delta of 1 means the call option is deep in the money and has a high probability of expiring in the money.

Put Options Delta:

Delta for put options typically ranges from 0 to -1.

A delta of 0 means the put option is out of the money and has a low probability of expiring in the money.

A delta of -1 means the put option is deep in the money and has a high probability of expiring in the money.

Delta is a dynamic parameter that changes as the price of the underlying asset, time to expiration, and volatility change. Here are a few key points to understand about delta:

Delta Neutrality: Traders often use delta to create delta-neutral positions, which means they aim to offset the directional risk in their portfolios. This can be achieved by combining options and their underlying assets in such a way that the total delta is close to zero.

Hedging with Delta: Delta can also be used for hedging. If an investor holds a stock position and wants to protect against a potential price decline, they may buy put options with negative delta to offset the positive delta of the stock.

Delta and Probability: Delta can be interpreted as an estimate of the probability that the option will expire in the money. For example, a delta of 0.30 can be seen as a 30% probability of the option expiring in the money.

Theta:

Negative Nature: Theta is always negative. This reflects the fact that, all else being equal, the time value of an option decreases as it approaches its expiration date. Therefore, the option premium tends to erode over time.

Impact on Option Premium: As time passes, the impact of theta becomes more pronounced, especially as the expiration date approaches. Options with a shorter time to expiration experience higher levels of time decay than those with more time until expiration.

Theta Decay Acceleration: Theta decay tends to accelerate as an option approaches expiration. In the early stages of an option’s life, theta decay is relatively slow, but it becomes more rapid in the final weeks and days before expiration.

Theta and Option Strategies: Traders and investors should be aware of theta when employing various option strategies. For example, when buying options, traders should consider the potential impact of time decay, and when selling options, they may seek to take advantage of time decay as a source of profit.

Theta and Delta Hedging: Theta is often a consideration in delta-hedging strategies. Traders may adjust their positions to maintain a desired delta while also managing the impact of time decay.

Gamma:

Dynamic Nature: Gamma is a dynamic parameter that changes as the price of the underlying asset changes. It is highest for at-the-money options and decreases as options move deeper in or out of the money.

Positive Nature: Gamma is always a positive value. This is because an increase in the price of the underlying asset tends to increase the absolute value of the delta for both call and put options. Conversely, a decrease in the underlying price tends to decrease the absolute value of the delta.

Impact on Delta: Gamma is closely related to delta. It represents the curvature of the option’s price curve. As the underlying asset moves, the delta of the option changes, and gamma measures how quickly that change occurs.

Gamma Acceleration: Similar to theta (time decay), gamma tends to increase as options approach their expiration dates. This means that near expiration, small price changes in the underlying asset can have a more significant impact on the option’s delta.

Gamma and Option Strategies: Traders and investors may consider gamma when constructing option strategies. For example, when using strategies like delta hedging, traders may adjust their positions to account for changes in gamma and its impact on delta.

Vega:

Positive Nature: Vega is always a positive value. This is because an increase in implied volatility generally leads to an increase in the option’s price, while a decrease in implied volatility tends to decrease the option’s price.

Impact of Implied Volatility: Higher implied volatility generally results in higher option premiums, reflecting the increased uncertainty or potential for larger price movements in the underlying asset. Lower implied volatility has the opposite effect.

Vega and Time to Expiration: Vega tends to be higher for options with more time until expiration. Longer-dated options are more sensitive to changes in volatility because they have more time for potential market fluctuations to occur.

Vega and Option Moneyness: At-the-money options typically have the highest vega, while in-the-money and out-of-the-money options have lower vega. This is because at-the-money options are more sensitive to changes in implied volatility.

Hedging with Vega: Traders and investors may use vega to manage their exposure to changes in volatility. For example, if they expect an increase in market volatility, they may increase their vega exposure by buying options to benefit from the potential rise in option prices.

Vega and Vega-Neutral Strategies: Some traders use vega-neutral strategies, where they try to offset positive and negative vega positions to reduce the impact of changes in implied volatility.

Rho:

Positive or Negative Rho: The sign of rho depends on whether the option is a call or a put:

For call options, rho is generally positive. This means that, all else being equal, the price of a call option is expected to increase with a rise in interest rates.

For put options, rho is generally negative. This implies that, all else being equal, the price of a put option is expected to decrease with a rise in interest rates.

Rho Sensitivity: Rho is often considered one of the least influential Greeks because interest rate changes, especially short-term changes, usually have a relatively small impact on option prices compared to factors like changes in the underlying asset’s price, volatility, or time decay.

Impact of Interest Rates: The relationship between interest rates and options prices is more noticeable for longer-dated options. As interest rates rise, the present value of future cash flows decreases, affecting the pricing of options with more extended expiration dates.

Rho and Option Maturity: Rho tends to be more significant for options with longer time to expiration. Shorter-dated options are less affected by changes in interest rates.

Practical Considerations: Traders and investors may not pay as much attention to rho compared to other Greeks, as interest rate changes are typically less frequent and less dramatic than other market factors.