Disclaimer: Davis Capital Research provides information and educational content related to stock trading for informational…

Carson DavisJanuary 21, 2024

Skip to main content

Skip to main content By definition:

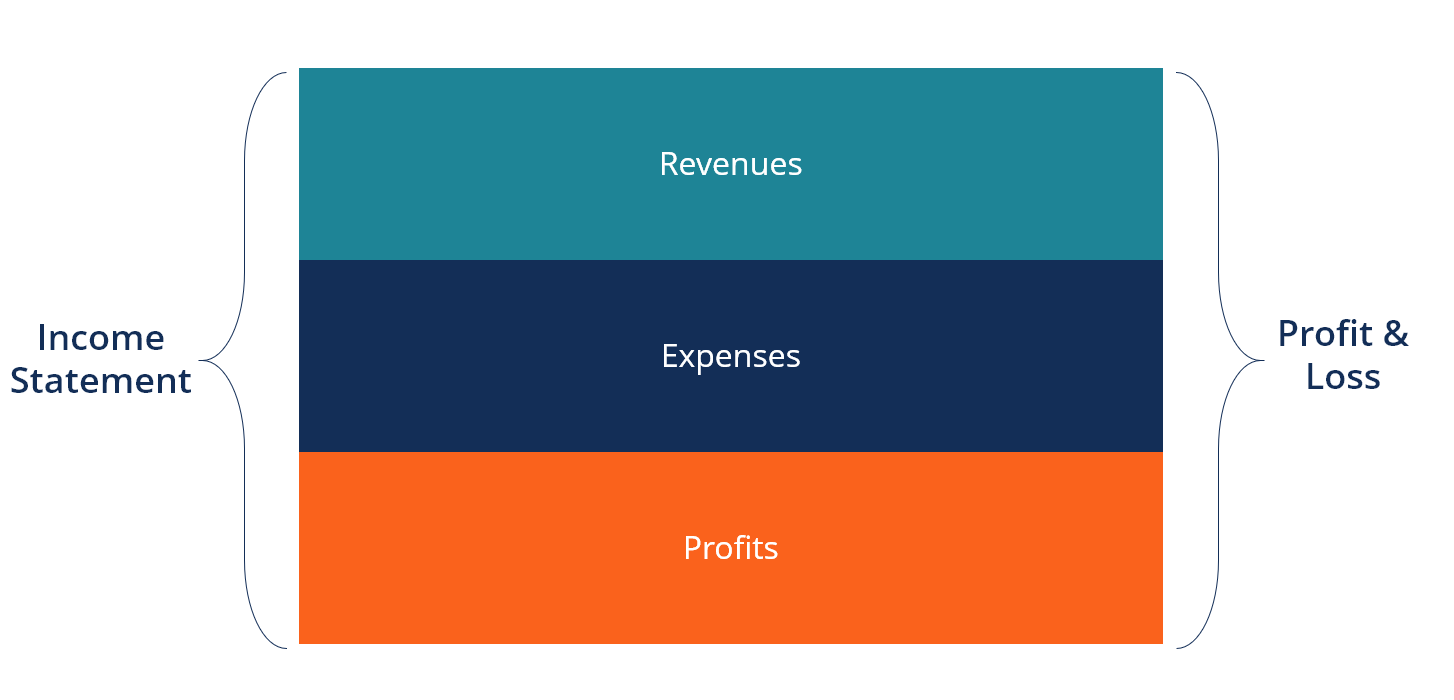

An income statement, also known as a profit and loss statement or statement of earnings, is a financial report that provides a summary of a company’s revenues, expenses, and profits over a specific period of time.

It is one of the three primary financial statements used by businesses, alongside the balance sheet and cash flow statement. The income statement helps stakeholders, such as investors, analysts, and managers, understand the financial performance of a company.

How do we use the income statement?

We use the income statement to evaluate the finnacial operations and efficiencies of the company.

Metrics like earnings as a ratio of revenue, earning per share (EPS), gross profit, gross profit margin, and expenses are all essential to evaluating the company and whether or not it is a good investment.

How is the income statement different from the balance sheet?

The primary differences between the income statement and the balance sheet are purpose and focus, time frame, and content. The balance sheet reflects the financial position at a certain point in time.

The income statement records the performance over a period of time (usually 1 year). The content of the income statement includes expenses and income. The balance sheet includes assets, liabilities, and equity.

The income statement measures profitability, the balance sheet measures the financial position.

Analyzing the income statement is crucial for various stakeholders, including investors, analysts, creditors, and management. Here are several key metrics we use to evaluate the income statement:

Gross Profit / Gross Profit Margin:

Gross Profit: Represents the actual profit generated from the core business activities, excluding operating expenses.

Gross Profit Margin: Expresses gross profit as a percentage of total revenue, providing a measure of the efficiency of the production process and profitability.

Both metrics are important for investors, analysts, and management to understand how well a company is performing in terms of producing and selling goods or services. A consistent or improving gross profit margin can be a positive sign, while a declining margin may indicate challenges in managing production costs or pricing strategies.

Earnings divided by revenue is a financial metric known as the earnings margin or profit margin. It is a measure of a company’s profitability and indicates the percentage of revenue that translates into earnings. There are different types of profit margins, and the specific term used may depend on what is included in the “earnings” or “profits.”

Net Profit Margin:

Formula: Net Profit Margin = (Net Income / Revenue) * 100

Explanation: Net profit margin represents the percentage of revenue that remains as net income (profit) after deducting all expenses, including cost of goods sold, operating expenses, interest, taxes, and other relevant costs.

Operating Profit Margin:

Formula: Operating Profit Margin = (Operating Income / Revenue) * 100

Explanation: Operating profit margin focuses on the profitability of a company’s core operations. It excludes interest and taxes from the calculation, providing a measure of how well a company is generating profit from its primary business activities.

Expenses is more of a subjective metric vs. the two prior. In general, we do not want to invest in companies that are spending money on R&D.

Why?

Because our primary focus is investing in companies with ESTABLISHED competitive advantages. If the company is spending a large portion of their income on R&D, it is unlikely the company holds a durable competitive advantage.

We also do not want to see high SG&A expenses. If income is rising, and SG&A is rising, notice the ratio of SG&A to income to determine if the company has their expenses in check.

This is perhaps a more controversial opinion here, but I would much rather invest in a company with stock-buy backs than a company issuing a high dividend. This is just a small fundamental analysis nuance that can tell a lot about a company

Stock Buybacks:

Companies may consider stock buybacks when they believe their stock is undervalued in the market. Repurchasing shares can be a way to signal confidence in the company’s future prospects.

Earnings Per Share (EPS) Improvement: Buybacks can enhance earnings per share (EPS) by reducing the number of outstanding shares. This is attractive to investors as it makes each remaining share more valuable.

Flexibility and Timing: Buybacks offer flexibility in terms of timing. Companies can execute buybacks when they have excess cash or believe that their stock is a good investment at the current market price.

Tax Efficiency: Buybacks are often more tax-efficient for shareholders than dividends, as capital gains taxes are typically lower than taxes on dividends.

Dividends:

Stable Income for Shareholders: Dividends provide a regular and stable income stream for shareholders. This can be particularly appealing to income-focused investors, such as retirees, who rely on dividend payments.

Signal of Financial Health: A consistent dividend payment is often seen as a sign of financial health and stability. It indicates that the company is generating sufficient profits and has confidence in its ability to maintain the payout.

Less Speculative: Dividends are considered less speculative than stock buybacks. Shareholders receive a direct cash payout, providing a tangible return on their investment.

Attracting Income Investors: Companies paying dividends may attract a different set of investors who prioritize income and are looking for reliable returns.

Factors Influencing the Decision:

Young, growth-oriented companies may prefer to reinvest profits into the business for expansion rather than distributing cash to shareholders. Mature companies with stable cash flows might be more inclined to return value through dividends or buybacks. The composition of a company’s investor base can influence the decision. If the majority of shareholders are income-focused, dividends may be preferred. If the focus is on capital appreciation, buybacks might be more suitable.

Companies with significant debt may opt for dividends to avoid increasing their leverage further. Buybacks, on the other hand, can be a way to return excess cash without committing to a regular payout. Tax implications for both the company and its shareholders play a role. Shareholders may prefer buybacks for potential tax advantages, while dividends could be more appealing in certain tax environments.

Ultimately, the decision to issue stock buybacks or dividends is influenced by a combination of the company’s financial health, growth strategy, investor expectations, and prevailing market conditions. Many companies also use a combination of both methods to strike a balance between returning value to shareholders and reinvesting in the business.

The income statement, also known as the profit and loss statement, provides a summary of a company’s revenues, expenses, and profits over a specific period. Here’s a comprehensive breakdown of the typical components found on an income statement:

Revenue (Sales): Represents the total amount of money generated from the sale of goods or services. Formula: Revenue = Quantity of Units Sold × Price per Unit

Cost of Goods Sold (COGS): Includes the direct costs associated with producing or delivering the goods or services sold.

Components may include raw materials, labor, and manufacturing overhead.

Formula: COGS = Opening Inventory + Purchases – Closing Inventory

Gross Profit: Calculated by subtracting the Cost of Goods Sold from total revenue.

Represents the profit before deducting operating expenses.

Formula: Gross Profit = Revenue – COGS

Operating Expenses: These are the ongoing costs of running the business, excluding the cost of goods sold.

Components include:Selling, General, and Administrative Expenses (SG&A), Marketing and Advertising Expenses, Research and Development Expenses, Depreciation and Amortization

Operating Expenses = SG&A + Marketing + R&D + Depreciation + Amortization

Operating Income (Operating Profit): Obtained by subtracting total operating expenses from gross profit.

Represents the profit generated from the company’s core operations.

Formula: Operating Income = Gross Profit – Operating Expenses

Other Income and Expenses: Includes non-operating items such as: Interest Income, Interest Expenses, Gains or Losses from the Sale of Assets.

Formula: Other Income and Expenses = Interest Income – Interest Expenses ± Gains/Losses

Income Before Tax: Obtained by adding or subtracting other income and expenses from operating income.

Represents the company’s total income before taxes are deducted.

Formula: Income Before Tax = Operating Income + Other Income and Expenses

Income Tax Expense: Represents the company’s tax obligation based on its taxable income. Calculated based on the applicable tax rate.

Formula: Income Tax Expense = Taxable Income × Tax Rate

Net Income (Net Profit or Net Earnings): The final amount after deducting income tax from income before tax.

Represents the overall profitability of the company.

Formula: Net Income = Income Before Tax – Income Tax Expense

The income statement provides a comprehensive overview of a company’s financial performance over a specific period. It is a crucial tool for investors, analysts, and management to assess profitability, operational efficiency, and overall financial health. Remember, technical analysis and fundemental analysis are completely different. The income statement is being used for fundamental analysis.

© 2024 Davis Capital Research. All Rights Reserved.

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator