Disclaimer: Davis Capital Research provides information and educational content related to stock trading for informational…

Carson DavisJanuary 21, 2024

Skip to main content

Skip to main content

The statement of cash flows is a financial statement that provides a summary of a company’s cash inflows and outflows over a specific period of time. It breaks down the cash flows into three main categories: operating activities, investing activities, and financing activities.

Operating activities: Operating activities section of the statement of cash flows reflects the cash inflows and outflows directly related to the core business operations of the company.

Investing activities: Investing activities section of the statement of cash flows reflects cash inflows and outflows related to the acquisition and disposal of long-term assets and investments that are not part of the company’s day-to-day operations.

Financing activities: Financing activities section of the statement of cash flows reflects cash inflows and outflows related to the company’s capital structure, including debt and equity financing, as well as distributions to shareholders.

The statement of cash flows is an essential component of a company’s set of financial statements, along with the other financial statements in fundamental analysis.

The statement of cash flows helps investors, analysts, and stakeholders understand how a company generates and uses cash. It provides insights into a company’s ability to meet its short-term obligations, invest in its operations, and return value to shareholders.

Additionally, it complements other financial statements by offering a more comprehensive view of a company’s financial health.

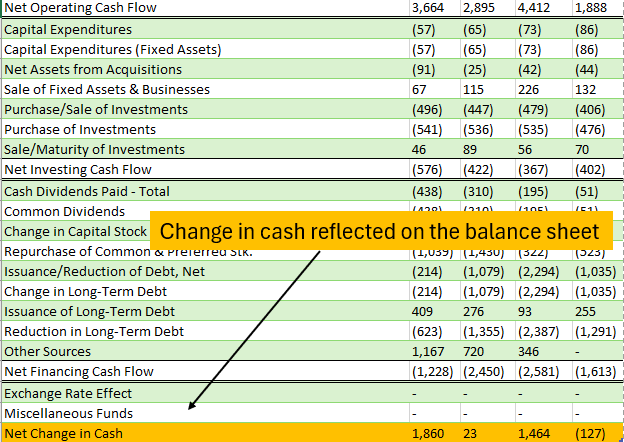

Notice in the image the net change in cash highlighted in yellow at the bottom. The net change in cash will also be reflected in the balance sheet as the year over year change in cash.

Also notice the three different sections. The operating section, the investing section, and the financing section. The statement of cash flows needs to be used in conjunction of the rest of your fundamental analysis.

Less than you think.

Many investors and analysts put a lot of weight into the companies free cash flow. While an important metric, we do not always care about free cash flow due to the different financial engineering that typically takes place.

What we mean is share repurchasing, dividends declared, and other items that effect the cash flow. Some of the best companies may report small cash flow amounts because they spend their money increasing shareholder value, which is what we are looking for! This can also make some figures within the income statement appear lower than they actually are.

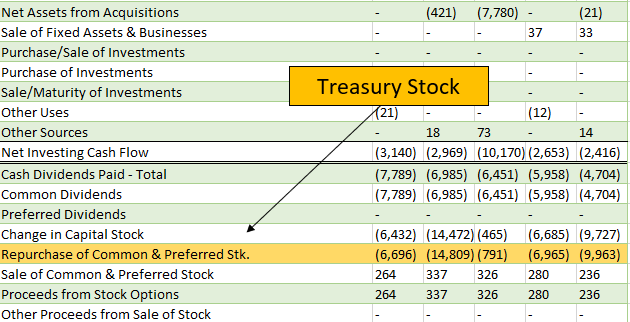

Share repurchasing activity is typically reflected in the financing activities section of the statement of cash flows. When a company repurchases its own shares, it involves cash transactions that affect the financing structure of the company.

Companies are paying cash to repurchase their shares and increase shareholder value.

Why would we look for this?

To put it plainly: If the company is struggling, or not economically rich, than they are most likely not issuing share repurchases. This is a trait typically seen by cash rich companies who then use the cash to increase shareholder value.

Find the companies share repurchasing account, if none, make sure cash flows are positive.

What does that mean? If the company is repurchasing shares, they are likely in a good economic state. If the company does not repurchase shares, or has no account related to the topic, then make sure the cash flows are positive. Even if the cash flows are positive, make sure to perform due diligence on the other financial statements.

Moody’s $MCO, is a great example of a company that is cash rich and is repurchasing shares to increase shareholder value.

They have been constantly repurchasing shares driving the price of the shares up as a result.

Key fundamentals about the Statement of Cash Flows:

The statement of cash flows stands as a fundamental pillar in the realm of financial reporting, offering a transparent depiction of a company’s cash movements over a specific period. This crucial financial statement provides investors, analysts, and stakeholders with insights into how a company generates and utilizes cash, thereby enhancing their understanding of its financial health and operational efficiency.

The statement of cash flows is structured into three primary categories: operating activities, investing activities, and financing activities. The operating activities section encapsulates cash transactions related to the company’s core business operations. It unveils the inflows from customer receipts, interest, and dividends, contrasting with outflows for payments to suppliers, employees, and various operating expenses. The net cash flow from operating activities serves as a barometer of a company’s ability to generate cash from its day-to-day operations.

Moving to the investing activities section, attention is directed towards the company’s capital allocation strategies. Here, cash flows associated with the acquisition and disposition of long-term assets take center stage. Positive inflows may arise from the sale of investments or property, while outflows occur when investing in new assets. The net cash flow from investing activities reflects the company’s commitment to long-term investments and divestment decisions.

Financing activities constitute the third component, shedding light on the company’s capital structure. Cash flows in this section stem from transactions with the company’s investors and creditors. The issuance of debt or equity results in cash inflows, while repayments and share repurchases translate into outflows. The net cash flow from financing activities illustrates the company’s financing decisions and their impact on its overall cash position.

Crucially, the statement of cash flows assists in evaluating a company’s liquidity, solvency, and financial strategy. A positive net cash flow signals robust operational performance and a capacity to meet short-term obligations. Conversely, a negative net cash flow raises questions about the sustainability of the company’s operations and its ability to navigate financial challenges.

Moreover, changes in the cash balance between the beginning and end of the reporting period offer a snapshot of the company’s financial trajectory. Stakeholders can discern whether the company is accumulating or depleting its cash reserves, influencing perceptions of its financial stability.

In conclusion, the statement of cash flows serves as a compass for navigating the financial landscape of a company. Its comprehensive breakdown of cash inflows and outflows across operating, investing, and financing activities empowers stakeholders to make informed decisions. As an indispensable companion to the income statement and balance sheet, the statement of cash flows completes the triad of financial statements, unveiling the intricate dance of cash within the intricate tapestry of corporate finance.

Cash is King:

The statement of cash flows focuses on cash movements, which is essential because cash is considered the lifeblood of a business. It reveals how effectively a company manages its cash resources, meets short-term obligations, and sustains its operations.

Operational Performance:

The operating activities section isolates cash flows directly related to the core business operations. By examining operating cash flow, analysts can evaluate the company’s ability to generate cash from its primary activities, providing insights into its operational efficiency and profitability.

Liquidity Assessment:

Fundamental analysis involves assessing a company’s liquidity, and the statement of cash flows is a key tool for this purpose. A positive net cash flow signals liquidity strength, indicating the ability to cover short-term obligations and invest in growth opportunities.

Investment and Financing Decisions:

Understanding the investing activities section helps analysts assess a company’s investment decisions. Positive cash flows from investing activities may indicate prudent investments, while negative cash flows may suggest divestment or capital expenditure commitments.

The financing activities section reveals how a company raises and returns capital. It sheds light on debt and equity financing, share repurchases, and dividend payments. Analysts can gauge the company’s capital structure and its approach to shareholder returns.

Insights into Capital Allocation:

Share repurchases and dividend payments are reflected in the statement of cash flows. Analysts can evaluate whether the company is returning value to shareholders through buybacks and dividends or if it is investing in growth opportunities.

Quality of Earnings:

The statement of cash flows complements the income statement by providing insights into the quality of earnings. It helps analysts discern whether reported profits on the income statement are backed by actual cash generation or if they are primarily accounting accruals.

Cash Conversion Cycle:

By examining the timing of cash inflows and outflows, analysts can assess the cash conversion cycle. This metric measures how quickly a company can convert its investments in inventory and accounts receivable into cash, providing a glimpse into working capital efficiency.

Predictive Value:

The statement of cash flows aids in forecasting future cash flows. Analysts can use historical cash flow patterns to make predictions about a company’s ability to sustain its operations, pay debts, and provide returns to shareholders.

In summary, the statement of cash flows is a critical tool in fundamental analysis as it provides a detailed and transparent view of a company’s cash-related activities. Analysts use this information to evaluate operational efficiency, liquidity, investment decisions, and the overall financial health of an asset, contributing to a comprehensive understanding of its intrinsic value and investment potential.

© 2024 Davis Capital Research. All Rights Reserved.

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator