Disclaimer: Davis Capital Research provides information and educational content related to stock trading for informational…

Carson DavisJanuary 21, 2024

Skip to main content

Skip to main content

Balance sheet defined:

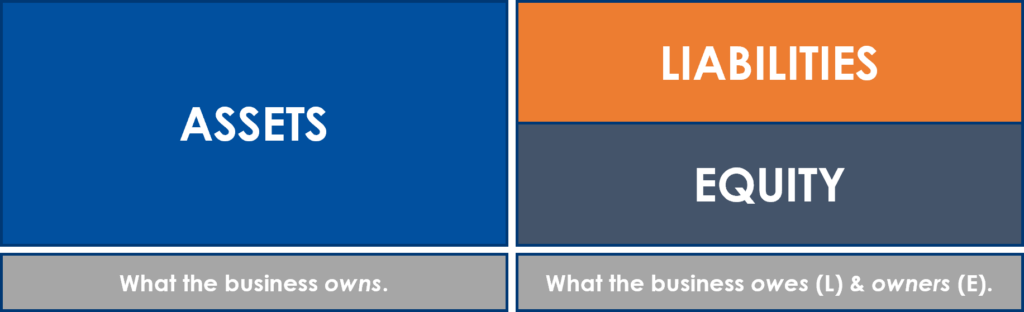

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a specific point in time. It consists of three main components: assets, liabilities, and equity. The balance sheet follows the accounting equation, which states that assets must equal liabilities plus equity.

Assets:

These are resources that the company owns or controls, and they are categorized into current assets and non-current assets. Current assets are those expected to be converted into cash or used up within one year, while non-current assets have a longer life.

Liabilities:

These represent the company’s obligations or debts and are also categorized into current liabilities and non-current liabilities. Current liabilities are those expected to be settled within one year, while non-current liabilities have a longer timeframe.

Equity:

Also known as shareholders’ equity or net assets, equity represents the residual interest in the company’s assets after deducting liabilities. It includes items such as common stock, retained earnings, and additional paid-in capital.

When using fundamental analysis, we are typically analyzing three financial statements. The three statements are the balance sheet, income statement, and the statement of cash flows. Each tells us important financial figures about the economic health of the company. When done properly, we can find companies that will create immense wealth for the shareholers.

The current ratio is a financial metric that measures a company’s ability to cover its short-term obligations with its short-term assets. It is calculated by dividing the total current assets by the total current liabilities.

The current ratio provides a quick assessment of a company’s short-term liquidity and its ability to meet its immediate financial obligations. A ratio above 1 indicates that the company has more current assets than current liabilities, suggesting it may be able to cover its short-term obligations. A ratio below 1 indicates potential liquidity issues.

Return on Assets (ROA) is a financial ratio that measures a company’s ability to generate profit from its assets. It is calculated by dividing the company’s net income by its average total assets.

Return on Assets is expressed as a percentage, and it represents the efficiency with which a company is utilizing its assets to generate profit. A higher ROA indicates that a company is more efficient in using its assets to generate earnings. ROA is used to compare companies within the same industry. It can be difficult to compare companies ROA if they are in completely different industries.

Return on Equity (ROE) is a financial ratio that measures the profitability of a company in relation to its shareholders’ equity. It indicates how efficiently a company is using its equity capital to generate profits.

Return on Equity is expressed as a percentage, and it provides insight into how well a company is utilizing the equity invested by its shareholders to generate profits. A higher ROE is generally considered favorable, as it indicates that the company is efficient in generating returns for its shareholders.

The debt-to-equity ratio is a financial metric that provides insight into a company’s capital structure by comparing its total debt to its shareholders’ equity. It is calculated by dividing total debt by shareholders’ equity.

The debt-to-equity ratio is expressed as a numerical ratio or percentage. It is used to assess the proportion of a company’s financing that comes from debt compared to equity.

Current Ratio Formula:

Current Assets / Current Liabilities

Debt to Equity Ratio Formula:

Total Debt / Shareholder’s Equity

Return on Assets:

Net Income / ((Beginning Assets + Ending Assets) / 2)

Return on Equity:

Net Income / Average Shareholder’s Equity

Cash: High cash likely means the company is performing well, which is good. Although we will make sure the company has not just sold bonds, as this can be a bad sign for our investment. High cash is great, but it is not essential to our decision making process.

PPE/Debt: We always want to see as little debt as possible. Typically, struggling or new companies will be carrying loads of debt on their balance sheets. If PPE (property, plant, and equipment) is > debt, it is likely the company is in some sort of good economic position.

ROA: Return on assets is always compared to companies within the same or similar industries. It would be near impossible to accurately compare a steel companies ROA to a software companies ROA. The two have such different structures and courses of normal business that they are likely to add more misleading figures when compared. The general rule here is higher the ROA the better.

Debt to Equity: A lot of great companies, the ones we are after, do not have a lot of long-term debt on their balance sheets. The companies we are after are usually so self-sufficient that they can self-finance themselves. These are the financial gold mines we are after. Any debt to equity less than 1 is fantastic.

Adjusted Debt to Equity: Adjusted debt to equity is when we add back treasury stock buy-backs to the equity formula. Treasury stock can be misleading, and when added back to the formula, it can tells us more about the companies economic position. It is one of our favorite techniques when finding great companies using fundamental analysis.

ROE: Companies that enjoy competitive advantages are likely to have high return on equity. The higher the ROE, the better.

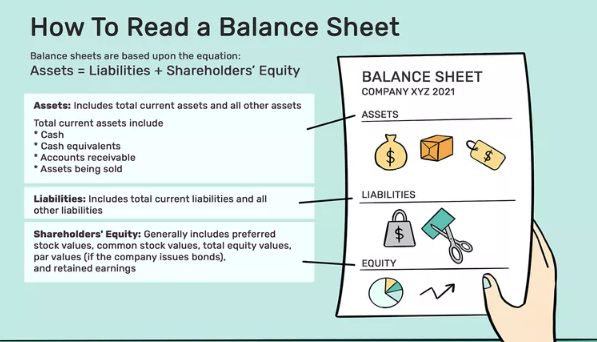

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a specific point in time. It consists of three main components: assets, liabilities, and equity. The balance sheet follows the accounting equation, which states that assets must equal liabilities plus equity.

Here’s a breakdown of the components of a balance sheet:

Assets: These are resources that the company owns or controls, and they are categorized into current assets and non-current assets.

Liabilities: These represent the company’s obligations or debts and are also categorized into current liabilities and non-current liabilities.

Equity: Also known as shareholders’ equity or net assets, equity represents the residual interest in the company’s assets after deducting liabilities. It includes items such as common stock, retained earnings, and additional paid-in capital.

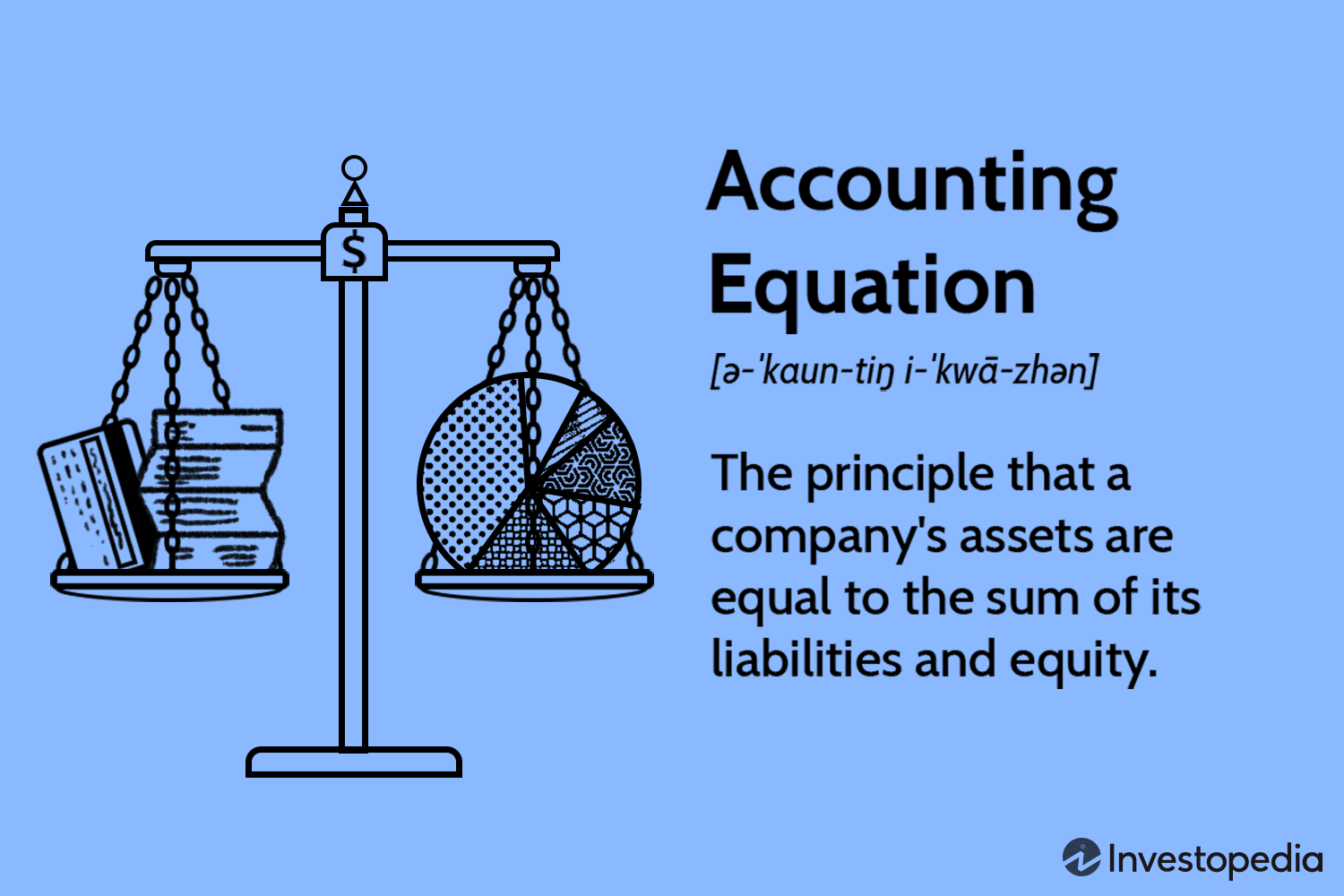

The balance sheet is based on the accounting equation: Assets= Liabilities+ Equity

This equation must always balance, ensuring that the company’s resources (assets) are financed by either debt (liabilities) or ownership (equity). The balance sheet provides valuable information about a company’s financial health, liquidity, and overall stability. It is an essential tool for investors, creditors, and analysts when assessing a company’s financial performance.

The current ratio is a financial metric that measures a company’s ability to cover its short-term obligations with its short-term assets. It is calculated by dividing the total current assets by the total current liabilities. The formula for the current ratio is:

Current Ratio = Current Assets / Current Liabilities

Here’s a breakdown of the components:

Current Assets: These are assets that are expected to be converted into cash or used up within one year. Examples include cash, accounts receivable, and inventory.

Current Liabilities: These are obligations or debts that are expected to be settled within one year. Examples include accounts payable, short-term debt, and other current liabilities.

The current ratio provides a quick assessment of a company’s short-term liquidity and its ability to meet its immediate financial obligations. A ratio above 1 indicates that the company has more current assets than current liabilities, suggesting it may be able to cover its short-term obligations. A ratio below 1 indicates potential liquidity issues.

Here’s how to interpret the current ratio:

Current Ratio > 1: Generally considered healthy, as it suggests the company has enough short-term assets to cover its short-term liabilities.

Current Ratio = 1: The company’s current assets are just enough to cover its current liabilities. While it meets its obligations, there is little room for unexpected events.

Current Ratio < 1: Indicates potential liquidity concerns, as the company may struggle to cover its short-term obligations with its current assets.

Return on Assets (ROA) is a financial ratio that measures a company’s ability to generate profit from its assets. It is calculated by dividing the company’s net income by its average total assets. The formula is:

ROA = Net Income / Average Total Assets

Here’s how to interpret Return on Assets:

Higher ROA: A higher percentage suggests that the company is effective in converting its assets into profits. It could indicate good management and operational efficiency.

Lower ROA: A lower percentage may suggest that the company is less efficient in using its assets to generate profits. This could be due to various factors, such as high operating expenses, inefficient asset utilization, or low-profit margins.

Return on Equity (ROE) is a financial ratio that measures the profitability of a company in relation to its shareholders’ equity. It indicates how efficiently a company is using its equity capital to generate profits. The formula is:

ROE = Net Income / Shareholder’s Equity

Here’s how to interpret Return on Equity:

Higher ROE: A higher percentage suggests that the company is effectively utilizing its equity to generate profits. It may indicate strong financial performance and efficient management.

Lower ROE: A lower percentage may suggest that the company is less efficient in using its equity to generate profits. This could be due to factors such as high debt levels, low-profit margins, or inefficient use of assets.

The debt-to-equity ratio is a financial metric that provides insight into a company’s capital structure by comparing its total debt to its shareholders’ equity. It is calculated by dividing total debt by shareholders’ equity.

The debt-to-equity ratio is expressed as a numerical ratio or percentage. It is used to assess the proportion of a company’s financing that comes from debt compared to equity. The interpretation of the ratio is as follows:

Low Debt-to-Equity Ratio: A ratio less than 1 suggests that the company has a lower level of debt relative to its equity. It may indicate a conservative capital structure, which could be less risky in terms of financial leverage.

High Debt-to-Equity Ratio: A ratio greater than 1 indicates that the company has a higher level of debt compared to equity. This might suggest a more leveraged capital structure, which can magnify returns but also increase financial risk.

© 2024 Davis Capital Research. All Rights Reserved.

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator